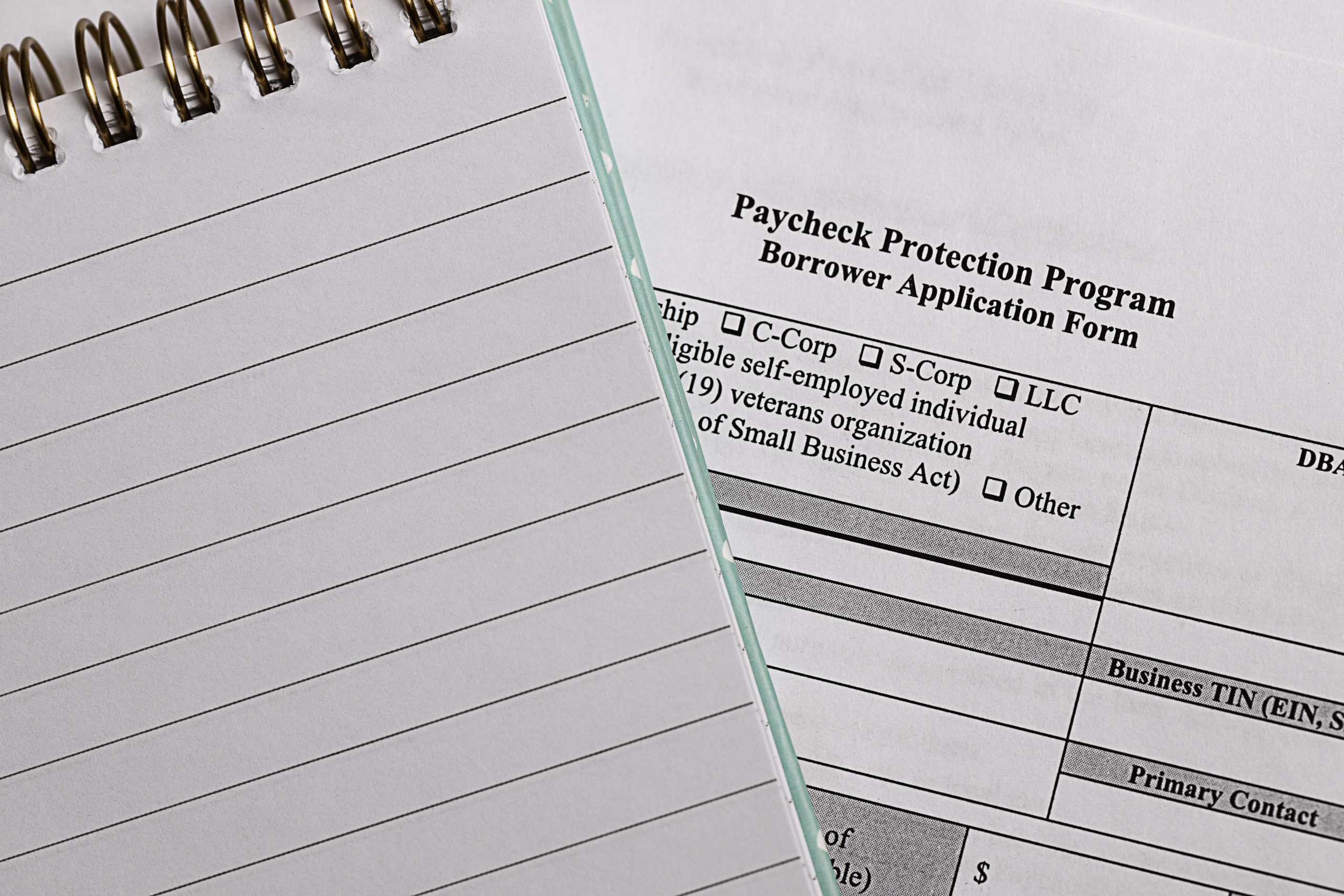

After the Federal government finally resolved the issue of the tax-deductibility of expenses paid using the proceeds of a forgiven Paycheck Protection Program (PPP) loan, taxpayers have waited to hear how the states would treat loan forgiveness and the related expenses. Most hoped it would be taxed similar to the favorable Federal treatment where the loan forgiveness is exempt from tax while the expenses paid with the loan proceeds still being allowed as a tax deduction. This alert will review the tax treatment of PPP loans for New Jersey, New York, and Pennsylvania along with other types of stimulus payments for which these states have provided guidance.

New Jersey

New Jersey recently passed legislation to address the taxability of PPP loans and expenses. For gross income tax (GIT) purposes, the bill specifically excludes PPP loan forgiveness from taxable income. The bill also provides that the PPP related expenses will be deductible for GIT purposes. For corporation business tax purposes, New Jersey generally follows Federal tax treatment therefore, PPP loan forgiveness will not be subject to tax and the expenses will be allowed as a deduction. New Jersey had previously announced that it would not tax the Federal Economic Stimulus Payments for GIT purposes.

New York

The New York Department of Taxation and Finance has issued guidance that New York will follow Federal tax treatment for PPP loan forgiveness and associated expenses. Therefore, the loan forgiveness will not be subject to tax and the expenses will remain deductible. Additionally, New York has provided that the Federal Economic Stimulus Payments are not subject to New York taxation as they are not included in Federal Adjusted Gross Income.

Pennsylvania

The Pennsylvania Department of Revenue has released guidance on the taxability of a number of CARES Act incentive provisions for personal and corporate tax purposes. Included in this guidance is the Pennsylvania tax treatment of PPP loan forgiveness and the related expenses. For personal tax purposes, any amount of PPP loan forgiveness will not be taxable income for personal tax purposes. Additionally, Pennsylvania has provided that no deduction will be disallowed for an expense that otherwise would qualify as deductible regardless of whether or not the expenses were paid for utilizing forgiven PPP loan proceeds.

Pennsylvania has also provided guidance on several other stimulus payments. Payments received by healthcare providers through the Provider Relief Fund will be considered nontaxable grants. This includes Health Resources and Service Administration claims reimbursements for uninsured patients. The advanced payment component of Economic Injury Disaster Loans will also be treated as a nontaxable grant. Additionally, the Federal Economic Impact Payments also known as stimulus checks will be viewed as a rebate and therefore not subject to tax.

Please contact your WG tax advisor for additional information regarding the state taxation of stimulus payments.