At the stroke of midnight on December 31, 2021, Internal Revenue Code Section 174, which has been a part of the tax code since 1954, will change significantly, and it will have an adverse impact to those businesses spending significant dollars on research and development. The provision, in its current state, generally provides businesses the ability to fully deduct the cost of its research and development activities (R&D) in computing taxable income in the year which the costs are incurred. This practice, called full expensing, without further legislative action, will expire effective December 31, 2021. The expiration of this beneficial provision will have immediate tax consequences to those companies that continue to invest in R&D activities.

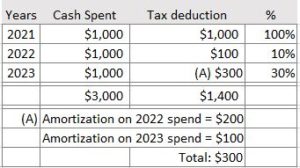

Written into the Tax Cuts and Jobs Act of 2017, changes to the rules under Section 174 will require taxpayers to subject their domestic R&D spend to a 5-year amortization period instead of the full immediate expensing under current law. Further, for those offshoring their R&D spend, the amortization period increases to 15 years. Let’s visualize the impact of these changes assuming Company A incurs $1,000 of annual domestic R&D spend for the following years:

The most striking impact of this rule change is evidenced by the 90% reduction in allowable R&D expensing between 2021 (pre-law change) and 2022 (post-law change). Additionally, despite the 5-year amortization period which would normally result in a deduction equal to 20%, the deduction for 2022 amortization is only 10%. Under the new rules, the amortization period begins at the midpoint of the year in which the R&D expenses are incurred, such that the first-year deduction post-2021 will be limited to 10% of the total R&D spend, and the amortization deductions will be spread over 7 years instead of 5 years.

There are many organizations projecting the economic impact of these changes on a domestic and global basis and although those opinions may differ, one fact remains consistent – 2022 will be more costly for U.S. companies investing in R&D. While tax planning should always be an ongoing process, if you are involved in R&D activities, the time to plan for these changes is now. Please contact your WG tax advisor.